Digitalisatie betekent het einde van het financiële departement, of toch niet?

Stel, u bent bijvoorbeeld een accountant, een financieel directeur of een financieel professional en u wilt uw impact vergroten op de organisatie. U ambieert een efficiënter financieel departement waarbij repetitief manueel werk gereduceerd wordt door gebruik te maken van nieuwe digitale technologieën. Dan is deze scriptie potentieel interessant voor u. Deze scriptie bevat een overzicht van de elementen die een invloed hebben op de mogelijkheid van het financieel departement om te digitaliseren.

Digitale technologieën in de financiële functie

De financiële functie in een organisatie omvat de financiële processen, de systemen en de werknemers die het financiële departement ondersteunen. Nieuwe digitale technologieën hebben een invloed op de processen en systemen van het financiële departement. McKinsey voorspelt dat digitale technologieën tot 50 procent van de financiële taken kunnen overnemen. Traditionele financiële taken kunnen worden geautomatiseerd, maar dat geeft de financiële functie ook de kans om haar rol in de organisatie te heroverwegen.

Wanneer wordt gesproken over nieuwe digitale technologieën, dan verwijst men vaak naar Artificiële Intelligentie (AI), robotisering, Internet of Things (IoT) en andere technologieën die deel uitmaken van de vierde industriële revolutie. Deze revolutie is mogelijk door de verhoogde computerkracht, versnelde gegevens verspreiding en cloud technologie. Slimme automatisatie, geavanceerde analytics en geïntegreerde systemen kunnen geïmplementeerd worden in het werk van de financiële functie. Het verwerken en analyseren van gegevens bijvoorbeeld wordt aanzien als een basisactiviteit van het financiële departement.

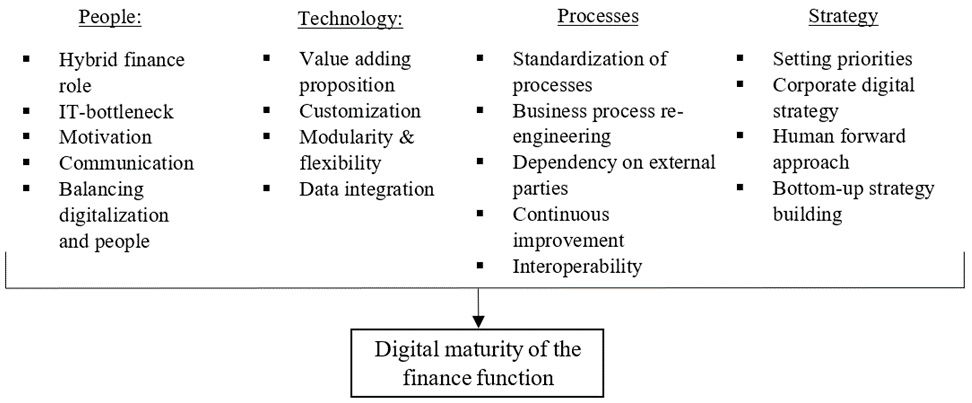

Digitale maturiteit van een financieel departement

De digitale maturiteit van een financieel departement kan verhoogd worden door de mensen, de technologieën, de processen en de strategie te optimaliseren.

Figuur 1 : Digitale maturiteit van de financiële functie

Figuur 1 geeft een overzicht van de elementen en de karakteristieken van digitale maturiteit voor de financiële functie. Financiële departementen met een hogere digitale maturiteit trekken financiële profielen aan met een digitale affiniteit en investeren in digitale technologieën. De standaardisatie van de financiële processen hebben invloed op de effectiviteit van de gebruikte digitale technologieën. De gebruikte technologieën in het financieel departement zijn modulair en flexibel. Als laatste zal de digitale strategie van de organisatie een invloed hebben op de digitale transformatie mogelijkheden van het financiële departement.

De rol van de werknemer in het digitale transformatieproces

De digitale kennis van de werknemers in het financiële departement heeft een invloed op de mate waarop de financiële functie een eigen digitale strategie kan uitbouwen. De digitale strategie van het financiële departement focust op het verhogen van kwaliteit en efficiëntie van de financiële taken. De werknemers van het financiële departement bezitten de digitale expertise om zich aan te passen aan de nieuwe digitale omgeving. De digitale onafhankelijk van het financiële departement tegenover het IT-departement verlaagt de IT-bottleneck. Een hybride financiële rol in het financiële departement kan de taak op zich nemen om een brug te vormen tussen het financiële en het IT-departement.

Digitalisatie als een nieuw begin voor de financiële functie

Digitalisatie betekent dus niet het einde van het financiële departement in een organisatie, maar geeft het departement de mogelijkheid om te focussen op waarde creërende taken. De financiële functie in een organisatie kan digitalisatie gebruiken als een hefboom om een nieuwe rol naar zich toe te trekken in een organisatie.

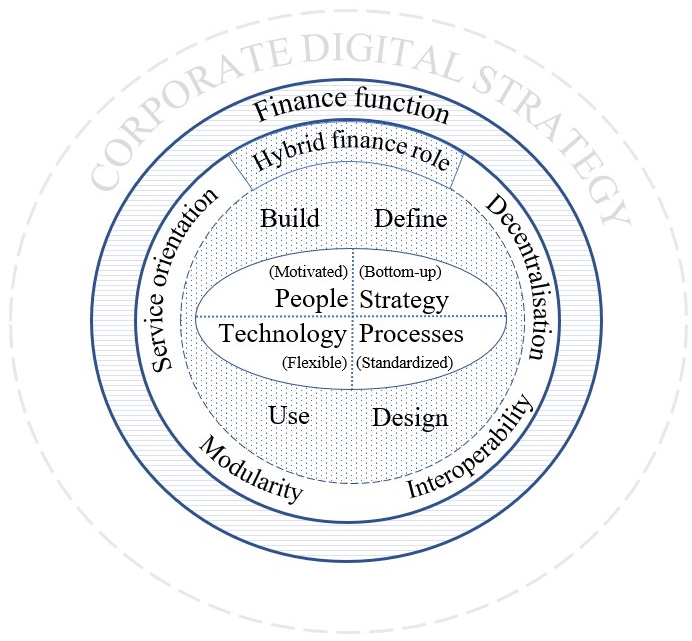

Figuur 2: De mogelijkheid van de financiële functie om te digitaliseren

Figuur 2 visualiseert de elementen die de financiële functie de mogelijkheid geven om te digitaliseren. De financiële functie in een organisatie ontwikkelt een digitale strategie van onderuit, maar is deels afhankelijk van de overkoepelde digitale strategie van de organisatie. Daarnaast kan een hybride rol de digitale expertise in het financiële departement verhogen en de digitale technologieën implementeren in het departement. De werknemers in het financiële departement bezitten een bepaalde digitale maturiteit om digitale prioriteiten te bepalen, maar dit is enkel mogelijk als de werknemer centraal staat in het digitale transformatieproces.

De complexiteit van de systemen en de processen hebben een invloed op de mogelijkheid van het financieel departement om te digitaliseren. Modulaire digitale technologieën laten de financiële functie toe om flexibel te werken en kosten te verlagen. De bedrijfsprocessen in de financiële functie moeten gestandaardiseerd worden om samenwerking en besluitvorming te bevorderen.

Bibliografie

ACCA (2013). Technology trends: their impact on the global accountancy profession. Retrieved April 3, 2019, from https://www.accaglobal.com/my/en/technical-activities/technical-resourc…

Aems, K. (2017). The future of finance: Using disruption to accelerate transformation. Retrieved January 19, 2019, from https://www.ibm.com/blogs/think/be-en/2017/12/20/future-finance-using-disruption-accelerate-transformation/

Allott, A., Weymouth, P., & Claret, J. (2001). Transforming the profession: management accounting is changing. Retrieved April 20, 2019, from https://www.cimaglobal.com/Global/UK/Employers/2000-12-31-transformingprofession_techrpt_1200.pdf

Bilstra, E. (2017). Op weg naar een high performance financiële functie. Retrieved February 2, 2019, from https://www.nba.nl/globalassets/over-de-nba/ledengroepen/aibs/dvf/eelco…;

Birt, J., Wells, P., Kavanagh, M., Robb, A., & Bir, P. (2018). Skills development: the digital age and opportunities for accountants. Retrieved January 11, 2019, from https://www.ifac.org/publications-resources/accounting-education-insights-ict-skills-development-0

Bloomberg, J. (2018). Digitization, Digitalization, And Digital Transformation: Confuse Them At Your Peril. Retrieved March 29, 2019, from https://www.forbes.com/sites/jasonbloomberg/2018/04/29/digitization-dig…

Boston Consultancy Group (2017). How Digital CFOs Are Transforming Finance. Retrieved December 26, 2019, from https://www.bcg.com/publications/2017/function-excellence-how-digital-c…

Boston Consultancy Group (2017). How Digital CFOs Are Transforming Finance. Retrieved January 19, 2019, from https://www.bcg.com/publications/2017/function-excellence-how-digital-c…

Caringe, A., & Holm, E. (2017). The Auditor’s Role in a Digital World : Empirical evidence on auditors’ perceived role and its implications on the principal-agent justification (Master’s dissertation, Uppsala University, Uppsala, Sweden). Retrieved March 15, 2019, from http://urn.kb.se/resolve?urn=urn:nbn:se:uu:diva-324752

Cerami M. (2017). Thriving in a Digital age. Retrieved January 13, 2019, from http://www.efaa.com/cms/upload/efaa_files/pdf/20170608_berlin_dtdp/20170608_session3_2_michael_cerami.pdf

Deloitte. (2015). Industry 4.0: Challenges and solutions for the digital transformation and use of exponential technologies. Retrieved March 2, 2019, from https://www2.deloitte.com/content/dam/Deloitte/ch/Documents/manufacturing/ch-en-manufacturing-industry-4-0-24102014.pdf

Deloitte. (2018). Finance 2025: Digital transformation in finance - Finance Transformation. Retrieved April 3, 2019, from https://www2.deloitte.com/be/en/pages/finance-transformation/articles/F…

Deloitte. (2018, December 11). Finance Digital Transformation: Predictions for 2025. Retrieved December 26, 2019, from https://www2.deloitte.com/us/en/pages/finance-transformation/articles/f…

European Union (2003). Commission Recommendation of 6 May 2003 concerning the definition of micro, small and medium-sized enterprises. Retrieved April 7, 2019, from https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32003H0361

Färm, J., & Jönsson, C. (2018). Shedding light on the controller profession : controllers’ value-creation in Swedish organizations (Master’s dissertation, Kristianstad University, Kristianstad, Sweden). Retrieved March 25, 2019 from http://urn.kb.se/resolve?urn=urn:nbn:se:hkr:diva-18558

Garg, N. K., Gupta, R. K., Jit, R., Bharti, A., & Gupta, N. (2018). Digitalization. Retrieved April 3, 2019, from https://www.researchgate.net/profile/Ishwar_Mittal/publication/32457143…

Gartner IT Glossary. (2012). Information technology. Retrieved March 27, 2019, from https://www.gartner.com/it-glossary/it-information-technology

Gartner IT Glossary. (2015). Digitalization. Retrieved March 24, 2019, from https://www.gartner.com/it-glossary/digitalization/

Gartner IT Glossary. (2018, May 25). Digitization. Retrieved March 24, 2019, from https://www.gartner.com/it-glossary/digitization

General Accounting Office (1990). Case study evaluations. Retrieved April 9, 2019 from https://www.gao.gov/special.pubs/10_1_9.pdf

Gill, M., & VanBoskirk, S. (2016). The digital maturity model 4.0. Benchmarks: Digital Transformation Playbook. Retrieved March 5, 2019, from https://forrester.nitro-digital.com/pdf/Forrester-s%20Digital%20Maturit…

International Business Machines (2017). The future of finance: Using disruption to accelerate transformation. Retrieved January 19, 2019, from https://www.ibm.com/blogs/think/be-en/2017/12/20/future-finance-using-d…

International Federation of Accountants (2006). Information Technology for Professional Accountants. Retrieved March 17, 2019, from https://www.ifac.org/system/files/meetings/files/2820.pdf

International Federation of Accountants Education Committee (IFAC) (s.d.). Information Technology for Professional Accountants. Retrieved on January 23, 2019, from https://www.imanet.org

Kristandl, G., Quinn, M., & Strauss, E. (2014). Management accounting and management control‐Cloud technology effects and a research agenda. Retrieved February 18, 2019, from https://gala.gre.ac.uk/id/eprint/14919/1/14919_Kristandl_Management%20a…

McKinsey (2016). Organization Agility and Organization Design. Retrieved April 2, 2019 from https://www.mckinsey.com/~/media/McKinsey/Business%20Functions/Organiza…

McKinsey (2018). Bots, algorithms, and the future of the finance function. Retrieved May 4, 2019, from https://www.mckinsey.com/business-functions/strategy-and-corporate-fina…

McKinsey (2018). Unlocking success in digital transformations. Retrieved March 15, 2019, from https://www.mckinsey.com/business-functions/organization/our-insights/u…

Niles, S. (2011). Standardization and modularity in data center physical infrastructure. Retrieved March 28, 2019, from https://www.schneider-electric.com/en/download/document/APC_VAVR-626VPD…

Oxford Dictionaries. (2018). Technology, Definition of technology in English. Retrieved March 27, 2019, from https://en.oxforddictionaries.com/definition/technology

Panetta, K. (2018). Gartner Top 10 Strategic Technology Trends for 2019. Retrieved February 2, 2019 from https://www.gartner.com/smarterwithgartner/gartner-top-10-strategic-tec…

PricewaterhouseCoopers (2015). Marktstudie financiële functie: Veranderen en vooruitkijken. Retrieved on February 25, 2019, from https://www.pwc.nl/nl/assets/documents/pwc-marktstudie-financiele-funct…

Rumpenhorst, F. (2016). Industry 4.0 building your digital enterprise. Price Waterhouse Coopers 2016 Global Industry 4.0 Survey. Retrieved March 5, 2019, from https://www.pwc.com/gx/en/industries/industries-4.0/landing-page/indust…

The Hackett Group. (2018). Robotic Process Automation. Retrieved February 15, 2019, from https://www.thehackettgroup.com/robotic-process-automation/

Adler, R., Everett, A.M. and Waldron, M. (2000), “Advanced management accounting techniques in manufacturing: utilization, benefits, and barriers to implementation”, Accounting Forum, Vol. 24 No. 2, pp. 131-150.

Aguirre, S., & Rodriguez, A. (2017). Automation of a business process using robotic process automation (rpa): A case study. In Workshop on Engineering Applications (pp. 65-71). Springer, Cham.

Ahmed, S. (2005). Desired competencies and job duties of non-profit CEOs in relation to the current challenges: Through the lens of CEOs' job advertisements. Journal of Management Development, 24(10), 913-928.

Ahrens, T., & Chapman, C. S. (2000). Occupational identity of management accountants in Britain and Germany. European Accounting Review, 9(4), 477-498.

Ahsan, K., Ho, M., & Khan, S. (2013). Recruiting project managers: A comparative analysis of competencies and recruitment signals from job advertisements. Project Management Journal, 44(5), 36-54.

Ala-Mutka, K. (2011). Mapping digital competence: Towards a conceptual understanding. Sevilla: Institute for Prospective Technological Studies.

Albers, A., Gladysz, B., Pinner, T., Butenko, V., & Stürmlinger, T. (2016). Procedure for defining the system of objectives in the initial phase of an industry 4.0 project focusing on intelligent quality control systems. Procedia Cirp, 52, 262-267.

Anagnoste, S. (2017). Robotic Automation Process-The next major revolution in terms of back office operations improvement. In Proceedings of the International Conference on Business Excellence (Vol. 11, No. 1, pp. 676-686). Sciendo.

Anderson, D. R. (1944). The function of industrial controllership. The Accounting Review, 19(1), 55–65.

Anderson, R. E. (2008). Implications of the information and knowledge society for education. In International handbook of information technology in primary and secondary education (pp. 5-22). Springer, Boston, MA.

Applegate, L. (1996). Managing in the Information Age. Boston, MA: Harvard Business School Press.

Armstrong, P (1985). Changing management control strategies: the role of competition between accountancy and other organisational professions. Accounting, Organisations and Society 10(2), 129–148.

Awayiga, J. Y., Onumah, J. M., & Tsamenyi, M. (2010). Knowledge and skills development of accounting graduates: The perceptions of graduates and employers in Ghana. Accounting Education: an international journal, 19(1-2), 139-158.

Bahador, K. M. K., & Haider, A. (2013). The Maturity of Information Technology Competencies: A Case of Accounting Practitioners in the Malaysian Accounting Service. In PACIS (p. 240).

Baldvinsdottir, G., Burns, J., Nørreklit, H., & Scapens, R. (2010). Professional accounting media: accountants handing over control to the system. Qualitative Research in Accounting & Management, 7(3), 395-414.

Baron, R. A., & Greenberg, J. (1990). Behavior in organizations. Boston: Allyn and Bacon.

Beattie, V., & Smith, S. J. (2013). Value creation and business models: refocusing the intellectual capital debate. The British Accounting Review, 45(4), 243-254.

Bhimani, A., & Bromwich, M. (2009). Management Accounting: retrospect and prospect. Elsevier.

Biddle, B. J. (1986). Recent developments in role theory. Annual review of sociology, 12(1), 67-92.

Bieńkowska, A., Kral, Z., & Zabłocka-Kluczka, A. (2017). IT tools used in the strategic controlling process–Polish national study results. In International Conference at Brno University of Technology, Faculty of Business and Management.

Brennen, J. S., & Kreiss, D. (2016). Digitalization. The international encyclopedia of communication theory and philosophy, 1-11.

Brewer, P. C., Sorensen, J. E., & Stout, D. E. (2014). The future of accounting education: Addressing the competency crisis. Strategic Finance, 96(2), 29-38.

Brynjolfsson, E., & Mcafee, A. (2017). The business of artificial intelligence. Harvard Business Review.

Burns, J., & Baldvinsdottir, G. (2005). An institutional perspective of accountants’ new roles—The interplay of contradictions and praxis. European Accounting Review, 14(4), 725–757.

Burns, J., & Baldvinsdottir, G. (2007). The changing role of management accountants. Issues in management accounting, 3, 117-132.

Byrne, S., & Pierce, B. (2007). Towards a more comprehensive understanding of the roles of management accountants. European Accounting Review, 16(3), 469-498.

Cadez, S., & Guilding, C. (2008). An exploratory investigation of an integrated contingency model of strategic management accounting. Accounting, organizations and society, 33(7-8), 836-863.

Caglio, A. (2003). Enterprise resource planning systems and accountants: towards hybridization?. European Accounting Review, 12(1), 123-153.

Cash, E., Yoong, P., & Huff, S. (2004). The impact of e-commerce on the role of IS professionals. ACM SIGMIS Database: the DATABASE for Advances in Information Systems, 35(3), 50-63.

Catlin, T., Scanlan, J., & Willmott, P. (2015). Raising your digital quotient. McKinsey Quarterly, 1-14.

Chang, H., Ittner, C. D., & Paz, M. T. (2014). The multiple roles of the finance organization: Determinants, effectiveness, and the moderating influence of information system integration. Journal of Management Accounting Research, 26(2), 1-32.

Chen, H., Chiang, R. H., & Storey, V. C. (2012). Business intelligence and analytics: From big data to big impact. MIS quarterly, 36(4).

Chong, V. K., & Monroe, G. S. (2015). The impact of the antecedents and consequences of job burnout on junior accountants' turnover intentions: a structural equation modelling approach. Accounting & Finance, 55(1), 105-132.

Chou, D. C., Bindu Tripuramallu, H., & Chou, A. Y. (2005). BI and ERP integration. Information Management & Computer Security, 13(5), 340-349.

Chowdhury, N. M. K., & Boutaba, R. (2009). Network virtualization: state of the art and research challenges. IEEE Communications magazine, 47(7), 20-26.

Colton, S. D. (2001). The changing role of the controller. Journal of Cost Management, 15(6), 5-16.

Cooper, P., & Dart, E. (2013). Business partnering as a complement to the accountant’s other roles: International survey evidence. Working paper, University of Bath, Bath.

Curtis, D. B., Hefley, W. E., & Miller, S. A. (2002). The people capability maturity model: Guidelines for improving the workforce. Addison-Wesley.

Dai, J., & Vasarhelyi, M. A. (2016). Imagineering Audit 4.0. Journal of Emerging Technologies in Accounting, 13(1), 1-15.

Davenport, T. H. (1993). Process innovation: reengineering work through information technology. Harvard Business Press.

Davenport, T. H., Harris, J. G., & Cantrell, S. (2004). Enterprise systems and ongoing process change. Business Process Management Journal, 10(1), 16-26.

Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS quarterly, 319-340.

de Bruin, T., Rosemann, M., Freeze, R., & Kulkarni, U. (2005). Understanding the main phases of developing a maturity assessment model. In 16th Australasian Conference on Information Systems, ACIS 2005.

de Waal, A. A. (2007). The characteristics of a high performance organization. Business Strategy Series, 8(3), 179-185.

de Waal, A., Bilstra, E., & De Roeck, P. (2019). Identifying the characteristics of a high-performance finance function. Journal of Advances in Management Research.

Derksen, B., & Luftman, J. (2013). Management and technology trends for IT executives. Compact International Magazine, 6-15.

DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American sociological review, 147-160.

Drath, R., & Horch, A. (2014). Industrie 4.0: Hit or hype?[industry forum]. IEEE industrial electronics magazine, 8(2), 56-58.

Jansen, E. P. (2018). Bridging the gap between theory and practice in management accounting: Reviewing the literature to shape interventions. Accounting, Auditing & Accountability Journal, 31(5), 1486-1509.

Edvinsson, L., & Sullivan, P. (1996). Developing a model for managing intellectual capital. European management journal, 14(4), 356-364.

Eisenhardt, K. M. (1989). Building theories from case study research. Academy of management review, 14(4), 532-550.

Favaro, P. (2001). Beyond bean counting: The CFO’s expanding role. Strategy & Leadership, 29(5), 4-8.

Fern, R. H., & Tipgos, M. A. (1988). Controllers as business strategists a progress report. Strategic Finance, 69(9), 25.

Fraser, P., Moultrie, J., & Gregory, M. (2002). The use of maturity models/grids as a tool in assessing product development capability. In IEEE international engineering management conference (Vol. 1, pp. 244-249). IEEE.

Freidson, E. (1999). Theory of professionalism: Method and substance. International review of sociology, 9(1), 117-129.

Frey, C. B., & Osborne, M. A. (2017). The future of employment: how susceptible are jobs to computerisation?. Technological forecasting and social change, 114, 254-280.

Friedman, A. L., & Lyne, S. R. (1997). Activity-based techniques and the death of the beancounter. European Accounting Review, 6(1), 19-44.

Gibbons, M., Limoges, C., Nowotny, H., Schwartzman, S., Scott, P., & Trow, M. (1994). The New Production of Knowledge: The Dynamics of Science and Research in Contemporary Societies. SAGE.

Goles, T., Hawk, S., & Kaiser, K. M. (2008). Information technology workforce skills: The software and IT services provider perspective. Information Systems Frontiers, 10(2), 179-194.

Goretzki, L., Strauss, E., & Weber, J. (2013). An institutional perspective on the changes in management accountants’ professional role. Management Accounting Research, 24(1), 41–63

Grabski, S. V., Leech, S. A., & Schmidt, P. J. (2011). A review of ERP research: A future agenda for accounting information systems. Journal of information systems, 25(1), 37-78.

Graham, A., Davey-Evans, S., & Toon, I. (2012). The developing role of the financial controller: evidence from the UK. Journal of Applied Accounting Research, 13(1), 71-88.

Granlund, M., & Lukka, K. (1998). It's a small world of management accounting practices. Journal of management accounting research, 10, 153.

Granlund, M., & Malmi, T. (2002). Moderate impact of ERPS on management accounting: a lag or permanent outcome?. Management accounting research, 13(3), 299-321.

Granlund, M., & Taipaleenmäki, J. (2005). Management control and controllership in new economy firms—a life cycle perspective. Management Accounting Research, 16(1), 21-57.

Hagel, J. (2012). New Skills for an Evolving Profession. Journal of Accountancy, 214(2), 24.

Hambrick, D. C., & Mason, P. A. (1984). Upper echelons: The organization as a reflection of its top managers. Academy of management review, 9(2), 193-206.

Hammer, M., & Stanton, S. (1999). How process enterprises really work. Harvard business review, 77, 108-120.

Herde, C. N., Wüstenberg, S., & Greiff, S. (2016). Assessment of complex problem solving: what we know and what we don’t know. Applied Measurement in Education, 29(4), 265-277.

Hermann, M., Pentek, T., & Otto, B. (2016). Design principles for industrie 4.0 scenarios. In 2016 49th Hawaii international conference on system sciences (HICSS) (pp. 3928-3937). IEEE.

Hirsch-Kreinsen, H. (2014). Smart production systems. A new type of industrial process innovation. In DRUID Society Conference (pp. 16-18).

Hoe, S. L. (2009). Transforming finance for the future. Journal of Organisational Transformation & Social Change, 6(1), 65-77.

Hoffjan, A. (2004), “The image of the accountant in a German context”, Accounting and the Public Interest, Vol. 4 No.1, pp. 62–89.

Hopper, T. M. (1980). Role conflicts of management accountants and their position within organisation structures. Accounting, Organizations and Society, 5(4), 401-411.

Hrisak, D. (1996). The controller as business strategist. Management Accounting (USA), 78(6), 48-50.

Hyvönen, T., Järvinen, J., & Pellinen, J. (2006). The role of standard software packages in mediating management accounting knowledge. Qualitative Research in Accounting & Management, 3(2), 145-160.

Iivari, M. M., Ahokangas, P., Komi, M., Tihinen, M., & Valtanen, K. (2016). Toward ecosystemic business models in the context of industrial internet. Journal of Business Models, 4(2).

Imran, M. (2018). Influence of Industry 4.0 on the Production and Service Sectors in Pakistan: Evidence from Textile and Logistics Industries. Social Sciences, 7(12), 246.

Iversen, K. L. (1998). The evolving role of finance. Strategy & Leadership, 26(2), 7-9.

Jablonsky, S. F., & Barsky, N. P. (2000). The digital workplace: how is it changing the role of financial management?. Journal of Corporate Accounting & Finance, 11(5), 3-12.

Jack, L., & Kholeif, A. (2008). Enterprise resource planning and a contest to limit the role of management accountants: a strong structuration perspective. In Accounting Forum (Vol. 32, No. 1, pp. 30-45). Elsevier.

Jackson, J. (1998). Contemporary criticisms of role theory. Journal of Occupational Science, 5(2), 49-55.

Järvenpää, M. (2007). Making business partners: a case study on how management accounting culture was changed. European Accounting Review, 16(1), 99-142.

Jayaram, A. (2016). Lean six sigma approach for global supply chain management using industry 4.0 and IIoT. In 2016 2nd International Conference on Contemporary Computing and Informatics (IC3I) (pp. 89-94). IEEE.

Johnson, A., Winter, P. A., Reio Jr, T. G., Thompson, H. L., & Petrosko, J. M. (2008). Managerial recruitment: the influence of personality and ideal candidate characteristics. Journal of Management Development, 27(6), 631-648.

Johnson, T. H., & Kaplan, R. S. (1987). Relevance lost: the rise and fall of management accounting. Boston: Harvard Business School Press

Kamble, S. S., Gunasekaran, A., & Gawankar, S. A. (2018). Sustainable Industry 4.0 framework: A systematic literature review identifying the current trends and future perspectives. Process Safety and Environmental Protection, 117, 408-425.

Katz, D., & Kahn, R. L. (1978). The social psychology of organizations. New York: Wiley.

Kerrigan, M. (2013). A capability maturity model for digital investigations. Digital Investigation, 10(1), 19-33.

Kim, J., Warga, E., & Moen, W. E. (2013). Competencies Required for Digital Curation: An Analysis of Job Advertisements. International Journal of Digital Curation, 8(1), 66-83.

Kochan, T. A., & Useem, M. (Eds.). (1992). Transforming organizations. Oxford University Press.

Kraut, A. I., Pedigo, P. R., McKenna, D. D., & Dunnette, M. D. (1989). The role of the manager: What's really important in different management jobs. Academy of Management Perspectives, 3(4), 286-293.

Kurunmäki, L. (2004). A hybrid profession—the acquisition of management accounting expertise by medical professionals. Accounting, organizations and society, 29(3-4), 327-347.

Lambert, C., & Sponem, S. (2012). Roles, authority and involvement of the management accounting function: a multiple case-study perspective. European Accounting Review, 21(3), 565-589.

Lasi, H., Fettke, P., Kemper, H. G., Feld, T., & Hoffmann, M. (2014). Industry 4.0. Business & information systems engineering, 6(4), 239-242.

Lee, H., Parsons, D., Kwon, G., Kim, J., Petrova, K., Jeong, E., & Ryu, H. (2016). Cooperation begins: Encouraging critical thinking skills through cooperative reciprocity using a mobile learning game. Computers & Education, 97, 97-115.

Legner, C., Eymann, T., Hess, T., Matt, C., Böhmann, T., Drews, P., Mädche, A., Urbach, N. & Ahlemann, F. (2017). Digitalization: opportunity and challenge for the business and information systems engineering community. Business & information systems engineering, 59(4), 301-308.

Lehrer, M., & Behnam, M. (2009). Modularity vs programmability in design of international products: Beyond the standardization–adaptation tradeoff?. European Management Journal, 27(4), 281-292.

Libby, T., & Waterhouse, J. H. (1996). Predicting change in management accounting systems. Journal of management accounting research, 8, 137.

Long, C. S., Ajagbe, A. M., Nor, K. M., & Suleiman, E. S. (2012). The approaches to increase employees’ loyalty: A review on employees’ turnover models. Australian Journal of Basic and Applied Sciences,, 6(10), 282-291.

Løwendahl, B. R., Revang, Ø., & Fosstenløkken, S. M. (2001). Knowledge and value creation in professional service firms: A framework for analysis. Human relations, 54(7), 911-931.

Lu, W. M. and Chen, M. H. (2011). A Benchmark Learning Roadmap for the Military Finance Center. Mathematical and Computer Modelling, 53 (9), pp. 1833-1843.

Lu, Y. (2017). Industry 4.0: A survey on technologies, applications and open research issues. Journal of Industrial Information Integration, 6, 1-10.

Lucia, A. D., & Lepsinger, R. (1999). Art & science of competency models. San Francisco, CA: Jossey-Bass.

Lukka, K. (2005). Approaches to case research in management accounting: the nature of empirical intervention and theory linkage. Accounting in Scandinavia–The Northern Lights, Liber & Copenhagen Business School Press, Kristianstad, SW, 375-99.

Lukka, K. (2014). Exploring the possibilities for causal explanation in interpretive research. Accounting, Organizations and Society, 39(7), 559-566.

Maas, V. S., & Matejka, M. (2009). Balancing the dual responsibilities of business unit controllers: Field and survey evidence. The Accounting Review, 84(4), 1233-1253.

Markus, M. L., & Robey, D. (1988). Information technology and organizational change: causal structure in theory and research. Management science, 34(5), 583-598.

Martin, A., & Grudziecki, J. (2006). DigEuLit: Concepts and tools for digital literacy development. Innovation in Teaching and Learning in Information and Computer Sciences, 5(4), 249-267.

Marx, F., Wortmann, F., & Mayer, J. H. (2012). A maturity model for management control systems. Business & information systems engineering, 4(4), 193-207.

Matt, C., Hess, T., & Benlian, A. (2015). Digital transformation strategies. Business & Information Systems Engineering, 57(5), 339-343.

Mettler, T., & Rohner, P. (2009). Situational maturity models as instrumental artifacts for organizational design. In Proceedings of the 4th international conference on design science research in information systems and technology (p. 22). ACM.

Mezulis, A. H., Abramson, L. Y., Hyde, J. S., & Hankin, B. L. (2004). Is there a universal positivity bias in attributions? A meta-analytic review of individual, developmental, and cultural differences in the self-serving attributional bias. Psychological bulletin, 130(5), 711–747.

Miles, R. E., Snow, C. C., Meyer, A. D., & Coleman Jr, H. J. (1978). Organizational strategy, structure, and process. Academy of management review, 3(3), 546-562.

Mohamad, S., Hendrick, M., O’Leary, C., & Best, P. (2014). Developing a model to evaluate the information technology competence of boards of directors. Corporate Ownership & Control, 12(1), 12.

Mohamed, E. K., & Lashine, S. H. (2003). Accounting knowledge and skills and the challenges of a global business environment. Managerial finance, 29(7), 3-16.

Moodley, M., & Saheed Bayat, M. (2017). Addressing the Causes and Failure for Financial Transformation while Achieving Business Alignment. Management Studies and Economic Systems, 3(3), 127-136.

Morgan, M. J. (2001). A new role for finance: Architect of the enterprise in the information age. Strategic Finance, 83(2), 36.

Mouritsen, J. (1996). Five aspects of accounting departments' work. Management Accounting Research, 7(3), 283-303.

Müller, J. M., Kiel, D., & Voigt, K. I. (2018). What drives the implementation of Industry 4.0? The role of opportunities and challenges in the context of sustainability. Sustainability, 10(1), 247.

Münstermann, B., Eckhardt, A., & Weitzel, T. (2010). The performance impact of business process standardization: An empirical evaluation of the recruitment process. Business Process Management Journal, 16(1), 29-56.

Newman, M., & Westrup, C. (2005). Making ERPs work: accountants and the introduction of ERP systems. European Journal of Information Systems, 14(3), 258-272.

Niven, P. R. (2002). Balanced scorecard step-by-step: Maximizing performance and maintaining results. John Wiley & Sons.

Noble, D. F. (1984). Forces of Production: A Social History of Industrial Automation. New York: Oxford University Press

Nolan, R. L. (1973). Managing the computer resource: a stage hypothesis. Communications of the ACM, 16(7), 399-405.

O'Donnell, D., Bontis, N., O'Regan, P., Kennedy, T., Cleary, P., & Hannigan, A. (2004). CFOs in e‐business: e‐architects or foot‐soldiers?. Knowledge and Process Management, 11(2), 105-116.

Orlikowski, W. J. (1992). The duality of technology: Rethinking the concept of technology in organizations. Organization science, 3(3), 398-427.

Parker, R. I., & Vannest, K. J. (2012). Bottom-up analysis of single-case research designs. Journal of Behavioral Education, 21(3), 254-265.

Parviainen, P., Tihinen, M., Kääriäinen, J., & Teppola, S. (2017). Tackling the digitalization challenge: How to benefit from digitalization in practice. International Journal of Information Systems and Project Management, 5(1), 63-77.

Paulk, M. C., Curtis, B., Chrissis, M. B., & Weber, C. V. (1993). Capability maturity model, version 1.1. IEEE software, 10(4), 18-27.

Pickard, M. D., & Cokins, G. (2015). From Bean Counters to Bean Growers: Accountants as Data Analysts—A Customer Profitability Example. Journal of Information Systems, 29(3), 151-164.

Pisching, M. A., Junqueira, F., Santos Filho, D. J., & Miyagi, P. E. (2015). An architecture for organizing and locating services to the industry 4.0. In Proceedings of 23rd ABCM international congress of mechanical engineering (p. 8).

Popovic, A., Coelho, P. M. P. S., & Jaklic, J. (2009). The impact of business intelligence system maturity on information quality. Information Research-An International Electronic Journal, 14(4), 1

Posada, J., Toro, C., Barandiaran, I., Oyarzun, D., Stricker, D., de Amicis, R., ... & Vallarino, I. (2015). Visual computing as a key enabling technology for industrie 4.0 and industrial internet. IEEE computer graphics and applications, 35(2), 26-40.

Ricciardi, V., & Simon, H. K. (2000). What is behavioral finance?. Business, Education & Technology Journal, 2(2), 1-9.

Rich, E. (1985). Artificial intelligence and the humanities. Computers and the Humanities, 19(2), 117-122.

Richins, G., Stapleton, A., Stratopoulos, T. C., & Wong, C. (2017). Big Data analytics: Opportunity or threat for the accounting profession?. Journal of Information Systems, 31(3), 63-79.

Rieg, R. (2018). Tasks, interaction and role perception of management accountants: evidence from Germany. Journal of Management Control, 1-38.

Ross, J. W. (2008). Creating a Strategic IT Architecture Competency: Learning in Stages. MIS Quarterly Executive, 2(1), 5.

Ross, J. W., Beath, C. M., & Sebastian, I. M. (2017). How to develop a great digital strategy. MIT Sloan Management Review, 58(2), 7.

Rüßmann, M., Lorenz, M., Gerbert, P., Waldner, M., Justus, J., Engel, P., & Harnisch, M. (2015). Industry 4.0: The future of productivity and growth in manufacturing industries. Boston Consulting Group, 9(1), 54-89.

Ryan, R. J., Scapens, R. W., & Theobald, M. (2002). Research methods and methodology in accounting and finance. Thomson, London.

Sabatier, P. A. (1986). Top-down and bottom-up approaches to implementation research: a critical analysis and suggested synthesis. Journal of public policy, 6(1), 21-48.

Samaranayake, P. (2009). Business process integration, automation, and optimization in ERP: Integrated approach using enhanced process models. Business Process Management Journal, 15(4), 504-526.

Santos, C., Mehrsai, A., Barros, A. C., Araújo, M., & Ares, E. (2017). Towards Industry 4.0: an overview of European strategic roadmaps. Procedia Manufacturing, 13, 972-979.

Sathe, V. (1983). The controller's role in management. Organizational Dynamics, 11(3), 31-48.

Sawyer, S., Eschenfelder, K. R., Diekema, A., & McClure, C. R. (1998). IT skills in the context of BigCo. In Proceedings of the 1998 ACM SIGCPR conference on Computer personnel research (pp. 9-18). ACM.

Scapens, R. W., & Jazayeri, M. (2003). ERP systems and management accounting change: opportunities or impacts? A research note. European accounting review, 12(1), 201-233.

Scarborough, H., & Corbett, J. M. (1992). Technology and organisation. Power, meaning and design. London: Routledge

Schafermeyer, M., Grgecic, D., & Rosenkranz, C. (2010). Factors influencing business process standardization: A multiple case study. In 2010 43rd Hawaii International Conference on System Sciences (pp. 1-10). IEEE.

Schäfermeyer, M., Rosenkranz, C., & Holten, R. (2012). The impact of business process complexity on business process standardization. Business & Information Systems Engineering, 4(5), 261-270.

Schumacher, A., Erol, S., & Sihn, W. (2016). A maturity model for assessing Industry 4.0 readiness and maturity of manufacturing enterprises. Procedia Cirp, 52, 161-166.

Sebastian, I. M., Ross, J. W., Beath, C., Mocker, M., Moloney, K. G., & Fonstad, N. O. (2017). How Big Old Companies Navigate Digital Transformation. MIS Quarterly Executive, 16(3), 6.

Sharma, R., & Jones, S. (2010). CFO of the future: strategic contributor or value adder?. Journal of Applied Management Accounting Research, 8(1), 1.

Snowden, D. (2002). Complex acts of knowing: paradox and descriptive self-awareness. Journal of knowledge management, 6(2), 100-111.

Somerville, M. M., Smith, G. W., & Smith Macklin, A. (2008). The ETS iSkillsTM Assessment: a digital age tool. The Electronic Library, 26(2), 158-171.

Spraakman, G., O'Grady, W., Askarany, D., & Akroyd, C. (2015). Employers’ perceptions of information technology competency requirements for management accounting graduates. Accounting Education, 24(5), 403-422.

Steenkamp, G. (2012). Student perceptions regarding the new training programme for chartered accountants. Journal of Economic and Financial Sciences, 5(2), 481-498.

Stock, T., & Seliger, G. (2016). Opportunities of sustainable manufacturing in industry 4.0. Procedia Cirp, 40, 536-541.

Stoner, G. (1999). IT is part of youth culture, but are accounting undergraduates confident in IT?. Accounting Education: An International Journal, 8(3), 217–237.

Tadeu, H. F. B., Duarte, A. L. D. C. M., Taurion, C., & Jamil, G. L. (2019). Digital Transformation: Digital Maturity Applied to Study Brazilian Perspective for Industry 4.0. In Best Practices in Manufacturing Processes (pp. 3-27). Springer, Cham.

Taipaleenmäki, J., & Ikäheimo, S. (2013). On the convergence of management accounting and financial accounting–the role of information technology in accounting change. International Journal of Accounting Information Systems, 14(4), 321-348.

Talwar, R. (1993). Business re-engineering—A strategy-driven approach. Long range planning, 26(6), 22-40.

Tam, T., (2013). What IT knowledge and skills do accounting graduates need?. New Zealand Journal Of Applied Business Research (NZJABR), 11(2), pp. 23-42.

ten Rouwelaar, J. A., Bots, J., & Vanamelsfort, M. (2008). Business unit controller involvement in management: An empirical study in the Netherlands. Available at SSRN 1277863.

Tucker, B.P. and Lowe, A.D. (2014), “Practitioners are from Mars; academics are from Venus? An investigation of the research-practice gap in management accounting”, Accounting, Auditing & Accountability Journal, Vol. 27 No. 3, pp. 394-425.

Tudor, C. G., Gheorghe, M., Oancea, M., & Robert, Ş. O. V. A. (2013). An analysis framework for defining the required IT&C competencies for the accounting profession. In Proceedings of the 8th International Conference on Accounting and Management Information Systems (AMIS 2013) (pp. 236-251).

Vaidya, S., Ambad, P., & Bhosle, S. (2018). Industry 4.0–a glimpse. Procedia Manufacturing, 20(1), 233-238.

Vakalfotis, N., Ballantine, J., & Wall, A. (2011). A literature review on the impact of enterprise systems on management accounting. In Proceedings of the 8th International Conference on Enterprise Systems, Accounting and Logistics (ICESAL) (pp. 11-12).

van Deursen, A. J. A. M. (2010). Internet Skills: Vital assets in an information society. Enschede: Universiteit Twente. https://doi.org/10.3990/1.9789036530866

Van Deursen, A. J. A. M., Helsper, E. J., & Eynon, R. (2014). Measuring digital skills. From Digital Skills to Tangible Outcomes project report. London: University of Twente.

Van Dijk, J., & Hacker, K. (2003). The digital divide as a complex and dynamic phenomenon. The information society, 19(4), 315-326.

Van Laar, E., van Deursen, A. J., van Dijk, J. A., & de Haan, J. (2017). The relation between 21st-century skills and digital skills: A systematic literature review. Computers in human behavior, 72, 577-588.

Verstegen, B., de Loo, I., Mol, P., Slagter, K., & Geerkens, H. (2007). Classifying controllers by activities: An exploratory study. Journal of Applied Management Accounting Research, 5(2), 9–32.

Vial, G. (2019). Understanding digital transformation: A review and a research agenda. The Journal of Strategic Information Systems. https://doi.org/10.1016/j.jsis.2019.01.003.

Wessels, P. L. (2005). Critical information and communication technology (ICT) skills for professional accountants. Meditari accountancy research, 13(1), 87-103.

Westerman, G., Tannou, M., Bonnet, D., Ferraris, P., & McAfee, A. (2012). The Digital Advantage: How digital leaders outperform their peers in every industry. MITSloan Management and Capgemini Consulting, MA, 2, 2-23.

Windeck, D., Weber, J., & Strauss, E. (2015). Enrolling managers to accept the business partner: the role of boundary objects. Journal of Management & Governance, 19(3), 617-653.

Wolf, S., Weißenberger, B. E., Claus Wehner, M., & Kabst, R. (2015). Controllers as business partners in managerial decision-making: Attitude, subjective norm, and internal improvements. Journal of Accounting & Organizational Change, 11(1), 24-46.

Xu, L. D., Xu, E. L., & Li, L. (2018). Industry 4.0: state of the art and future trends. International Journal of Production Research, 56(8), 2941-2962.

Yazdifar, H., Askarany, D., & Askary, S. (2008). Management accountants' role in dependent and independent companies: does ownership matter?. Journal of Accounting-Business & Management, 15(2).

Yin, R. K. (1981). The case study as a serious research strategy. Knowledge, 3(1), 97-114.

Yin, R.K. (2009). Case Study Research: Design and Methods. Sage, Beverly Hills, CA 5

Zainuddin, Z. N., & Sulaiman, S. (2016). Challenges faced by management accountants in the 21st century. Procedia Economics and Finance, 37, 466-470.

Zoni, L., & Merchant, K. A. (2007). Controller involvement in management: an empirical study in large Italian corporations. Journal of Accounting & Organizational Change, 3(1), 29-43.

Zoni, L., & Pippo, F. (2017). CFO and finance function: what matters in value creation. Journal of Accounting & Organizational Change, 13(2), 216-238.

Zuboff, S. (1988). In the age of the smart machine: The future of work and power (Vol. 186). New York: Basic books.

Zwieg, P., Kaiser, K. M., Beath, C. M., Bullen, C., Gallagher, K. P., Goles, T., ... & Carmel, E. (2006). The information technology workforce: Trends and implications 2005-2008. MIS Quarterly Executive, 5(2), 47-54.