Financiële crashes kunnen tot het verleden behoren door de hulp van Artificiële Intelligentie

Fragiliteit is inherent aan het financieel systeem door doorgedreven globalisatie

Met het vallen van de Berlijnse muur is de globalisering in een stroomversnelling gekomen . Een proces die al in gang was gezet na het einde van de Tweede Wereldoorlog. Een belangrijk fundament van die globalisatie is de internationale verwevenheid van het financiële systeem, die geholpen heeft de koopkracht naar ongeziene hoogtes te stuwen. Dit betekent dat bijvoorbeeld het risico van een lening uitgeschreven in de Verenigde Staten kan gedragen worden door een Belgische spaarbank. De Belgische bank moet daar weinig kapitaal tegenover staan hebben aangezien het portfolio als gediversifieerd kan beschouwd worden. Bijgevolg kunnen actoren in het financieel systeem onder het mom van diversificatie hun balansen aandikken en hoge winsten boeken.

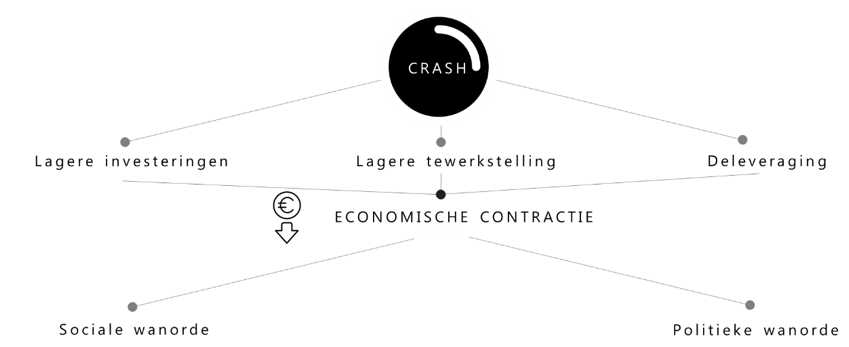

De assumptie van diversificatie is geen pure larie en apekool en houdt weldegelijk steek onder ‘normale’ omstandigheden’. Bij een situatie waar een deel van het financiële systeem onder stress staat is dat echter niet meer het geval. Toch weigert men vaak die basisassumptie te laten varen onder het mom van ‘this time is different’. Onder stress scenario’s laten actoren hun rationele assumpties varen en vluchten de deur uit als een kudde schapen achter nagezeten door een hond, en trachten ze te redden wat te redden valt. Ex-post benoemen financiële journalisten en academici dit gegeven als een geklapte bubbel of crash Een dergelijke situatie die begint als overspeculatie in een bepaald activa segment, kan het hele financiële systeem besmetten met potentiële desastreuze gevolgen voor de reële economie. Extreme werkloosheid, gigantische overheidsschulden en faillissementen behoren tot deze mogelijke consequenties.

Figuur 1: Crashes hebben 2de en 3de orde consequenties op de reële economie

Voorspellen van een bubbel en de daarbij horende crashes zou potentieel desastreuse gevolgen voor de reële economie kunnen voorkomen

De vraag rijst nu of dergelijk crashes voorspeld kunnen worden en door arbitrage kunnen verhinderd worden. De logica is als volgt. Wanneer je weet dat er een bubbel op klappen staat, speculeer je dat de prijs van het activa gaat dalen door het activa te verkopen. Dit zorgt dat de prijs daalt en de bubbel verhindert wordt.

Veel professionelen en academici hebben hun tanden (tevergeefs) stuk gebeten op dit vraagstuk. De vierde industriële revolutie, en meer specifiek, het toegankelijk worden van artificiële intelligentie, biedt nieuwe opportuniteiten om deze kwestie te tackelen.

Deze scriptie surft mee op de recentste evoluties in artificiële intelligentie en doet een poging crashes te voorspellen in allerlei activa klassen. Artificiële intelligentie toont enkel superieure prestaties wanneer het massale hoeveelheden data kan analyseren (daarom wordt het vaak het broertje van de big data revolutie genoemd). Het uitzonderlijk karakter van crashes heeft echter als gevolg dat er weinig gedocumenteerde crashes zijn. Deze scriptie heeft dit obstakel trachten te overkomen door zelf data te genereren die eigenschappen vertonen gelijkaardig aan de eigenschappen vertoont door activa klassen die leiden tot een crash.

Het eerste deel is gewijd aan het vinden van een model capabel om synthetische data te genereren die zo dicht mogelijk aanleunt bij synthetische data. In het tweede deel wordt het AI model losgelaten op de miljoenen reeksen synthetische data met als doel dat het AI model de nuances leert tussen reeksen die uitmonden in een crash en geen crash. In het laatste deel wordt het AI model dat die nuances leerde losgelaten op echte prijsreeksen om te kijken of het er in slaagt ook in echte financiële tijdreeksen crashes te voorspellen.

Figuur 2: Structuur van het werk

Genereer synthetische data om miljoenen prijsverlopen te genereren die crashes bevatten

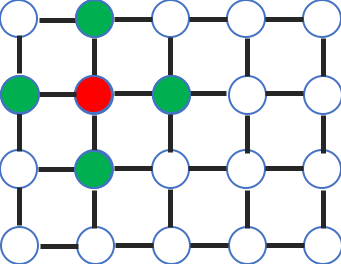

Het model dat financiële synthetische data genereert, moest aan enkele voorwaarden voldoen. De belangrijkste eigenschap de aanwezigheid van fat tails. Fat tails is een statistische eigenschap die de aanwezigheid van crashes aanduidt. Het uiteindelijke model is gebaseerd op inzichten in de statistische fysica, waarbij financiële actoren in een netwerk werden gesimuleerd. Alle agenten oefenen in een zekere mate invloed op elkaar uit. Op een bepaald moment is de invloed gestegen in die mate dat iedereen elkaar imiteert. Wanneer enkele agenten beseffen dat bepaalde activa aan redeloze prijzen handelen, verkopen ze massaal hun activa. Door de hoge mate van imitatie verkopen de rest van de agenten mee met een crash als gevolg.

Train een AI-model om de nuances in de synthetische data te leren tussen prijsverlopen die uitmonden in crashes en niet uitmonden in crashes

Nadat dit agenten-model miljoenen prijsverlopen heeft gesimuleerd (bv. het prijsverloop van goud of van het aandeel Bekaert). Wordt er in de tweede fase een AI model getraind die moet trachten te onderscheiden of een bepaalde reeks in de nabije toekomst zal uitmonden in een crash.

Figuur 3: De mening van elke agent wordt beïnvloed door zijn naaste buren. Dit fenomeen veroorzaakt imitatie gedrag wat tot crashes leidt.

Het model loslaten op echte financiële tijdreeksen toont het potentieel van de onderzoeksaanpak

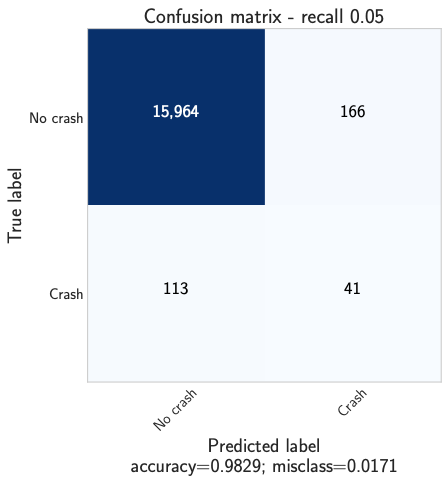

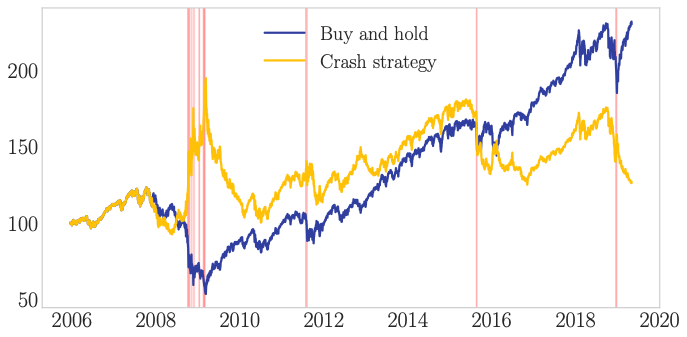

Het model slaagt er in om van de 164 ongecorreleerde crashes van de afgelopen 10 jaar, over verschillende activa klassen, er 41 te voorspellen waaronder de desastreuse crash in 2008. Verder zag het model 166 keer een crash aankomen die er uiteindelijk niet kwam. Wanneer we op deze informatie zouden gehandeld op bijvoorbeeld de S&P 500 en telkens ‘short’ gegaan zijn wanneer het model een crash voorspelt en ‘long ‘ wanneer het model geen crash voorspelt, zouden we op verschillende momenten de markt verslaan. Dit is een veelbelovend resultaat die voor verschillende actoren van nut kan zijn om hun risico te managen en als fundament kan dienen voor verder onderzoek.

Figuur 4: Van de 200 ongecorreleerde crashes, kan het model er 40 voorspellen. 166 keer voorspelt het model een crash dat uiteindelijk niet tot uiting komt

Figuur 5: Cumulatieve returns van een trading strategie gebaseerd op het model versus buy and hold van de S&P 500

Bibliografie

Alstott, J., Bullmore, E., and Plenz, D. (2014). “powerlaw: A Python Package for Analysis of Heavy-Tailed Distributions”. In: PLoS ONE 9.1, e85777. doi: 10.1371/journal. pone.0085777. arXiv: 1305.0215 [physics.data-an]. Arisue, H. and Tabata, K. (2001). “First Order Phase Transition of the Q-State Potts Model in Two Dimensions”. In: Non-Perturbative Methods and Lattice QCD, pp. 233– 241. doi: 10.1142/9789812811370_0024. arXiv: hep-lat/0007025 [hep-lat]. Aste, T. (2013). Stylized facts of financial data. url: https : / / wiki . ucl . ac . uk / display/FinSci/Stylized%20facts%20of%20financial%20data. Balanda, K. and Macgillivray, H. (1988). “Kurtosis: A Critical Review”. In: The Americal Statistician 42, pp. 111–119. doi: 10.1080/00031305.1988.10475539. Bar-Yam, Y. and Kantor, D. (2018). “A Mathematical Theory of Interpersonal Interactions and Group Behavior”. In: arXiv e-prints, arXiv:1812.11953, arXiv:1812.11953. arXiv: 1812.11953 [physics.soc-ph]. Bengio, Y., Simard, P., Frasconi, P., et al. (1994). “Learning long-term dependencies with gradient descent is difficult”. In: IEEE transactions on neural networks 5.2, pp. 157–166. Blanchard, O. and Watson, M. (1982). Bubbles, Rational Expectations and Financial Markets. NBER Working Papers 0945. National Bureau of Economic Research, Inc. url: https://EconPapers.repec.org/RePEc:nbr:nberwo:0945. Bornholdt, S. (2001). “Expectation Bubbles in a Spin Model of Markets”. In: International Journal of Modern Physics C 12, pp. 667–674. doi: 10.1142/S0129183101001845. arXiv: cond-mat/0105224 [cond-mat.stat-mech].

Bouchaud, J.-P., Matacz, A., and Potters, M. (2001). “Leverage effect in financial markets: The retarded volatility model”. In: Physical review letters 87.22, p. 228701. Bouri, E., Gupta, R., and Roubaud, D. (2018). “Herding behaviour in cryptocurrencies”. In: Finance Research Letters. issn: 1544-6123. doi: https://doi.org/10.1016/j. frl.2018.07.008. url: http://www.sciencedirect.com/science/article/pii/ S1544612318303647. Bradley, A. P. (1997). “The use of the area under the ROC curve in the evaluation of machine learning algorithms”. In: Pattern recognition 30.7, pp. 1145–1159. Brée, D. S., Challet, D., and Peirano, P. P. (2013). “Prediction accuracy and sloppiness of log-periodic functions”. In: Quantitative Finance 13.2, pp. 275–280. Bree, D. S. and Lael Joseph, N. (2010). “Fitting the Log Periodic Power Law to financial crashes: a critical analysis”. In: arXiv e-prints, arXiv:1002.1010, arXiv:1002.1010. arXiv: 1002.1010 [q-fin.ST]. Buckland, M. and Gey, F. (1994). “The relationship between recall and precision”. In: Journal of the American society for information science 45.1, pp. 12–19. Buda, M., Maki, A., and Mazurowski, M. A. (2017). “A systematic study of the class imbalance problem in convolutional neural networks”. In: CoRR abs/1710.05381. arXiv: 1710.05381. url: http://arxiv.org/abs/1710.05381. Campbell, J. et al. (1997). The Econometrics of Financial Markets. Princeton University Press. isbn: 9780691043012. url: https : / / books . google . be / books ? id = lkeKhnqUHx8C. Chancellor, E. (1999). Devil take the hindmost : a history of financial speculation / Edward Chancellor. English. 1st ed. Farrar, Straus, Giroux New York, xiv, 386 p. cm. isbn: 0374138583. Chang, G. and Feigenbaum, J. (2006). “A Bayesian analysis of log-periodic precursors to financial crashes”. In: Quantitative Finance 6.1, pp. 15–36. Charles P. Kindleberger, R. Z. A. (1978). Manias, panics and Crashes. Vol. 7. Palgrave Macmillan, pp. 38–53. Chen, J., Hong, H., and Stein, J. C. (2002). “Breadth of Ownership and Stock Returns”. In: Journal of Financial Economics 66.November-December, pp. 171–205.

Cho, J. et al. (2015). “How much data is needed to train a medical image deep learning system to achieve necessary high accuracy?” In: arXiv preprint arXiv:1511.06348. Chollet, F. et al. (2015). Keras. https://keras.io. Chordia, T., Roll, R., and Subrahmanyam, A. (2008). “Liquidity and market efficiency”. In: Journal of Financial Economics 87.2, pp. 249–268. Clauset, A., Shalizi, C. R., and Newman, M. E. (2009). “Power-law distributions in empirical data”. In: SIAM review 51.4, pp. 661–703. Cont, R. (2001a). “Empirical properties of asset returns: stylized facts and statistical issues”. In: Quantitative Finance 1.2, pp. 223–236. doi: 10.1080/713665670. eprint: https://doi.org/10.1080/713665670. url: https://doi.org/10.1080/713665670. Cont, R. (2001b). “Empirical properties of asset returns: stylized facts and statistical issues”. In: Cruz, R. et al. (2016). “Tackling class imbalance with ranking”. In: 2016 International joint conference on neural networks (IJCNN). IEEE, pp. 2182–2187. Davis, J. and Goadrich, M. (2006). “The relationship between Precision-Recall and ROC curves”. In: Proceedings of the 23rd international conference on Machine learning. ACM, pp. 233–240. Delong, J. B., Stuart, J., and Marshall, A. (2009). “The Simplest Possible Behavioral Finance Bubble Model”. In: The Economist, pp. 1–12. url: http://citeseerx.ist. psu.edu/viewdoc/download?doi=10.1.1.186.834&rep=rep1&type=pdf. Depken, C. A., Hollans, H., and Swidler, S. (2011). “Flips, flops and foreclosures: anatomy of a real estate bubble”. In: Journal of Financial Economic Policy 3.1, pp. 49– 65. doi: 10.1108/17576381111116759. eprint: https://doi.org/10.1108/17576381111116759. url: https://doi.org/10.1108/17576381111116759. Drummond, C. and Holte, R. C. (2000). “Exploiting the Cost (In)Sensitivity of Decision Tree Splitting Criteria”. In: Proceedings of the Seventeenth International Conference on Machine Learning. ICML ’00. San Francisco, CA, USA: Morgan Kaufmann Publishers Inc., pp. 239–246. isbn: 1-55860-707-2. url: http://dl.acm.org/citation.cfm?id= 645529.658143. Egan, J. P. (1975). “Signal detection theory and {ROC} analysis”. In:

Enric, C. (2017). “Computational Physics”. In: pp. 34–35. url: http : / / itf . fys . kuleuven.be/~enrico/Teaching/monte_carlo_2018.pdf. Fama, E. F. (1965). “The Behavior of Stock-Market Prices”. In: The Journal of Business 38.1, pp. 34–105. issn: 00219398, 15375374. url: http://www.jstor.org/stable/ 2350752. Fan, J. and Yao, Q. (2017). The Elements of Financial Econometrics. The Elements of Financial Econometrics. Cambridge University Press, pp. 20–23. isbn: 9781107191174. url: https://books.google.be/books?id=7N0cDgAAQBAJ. Fawcett, T. (2006). “An Introduction to ROC Analysis”. In: Pattern Recogn. Lett. 27.8, pp. 861–874. issn: 0167-8655. doi: 10.1016/j.patrec.2005.10.010. url: http: //dx.doi.org/10.1016/j.patrec.2005.10.010. Filimonov, V. and Sornette, D. (2013). “A stable and robust calibration scheme of the log-periodic power law model”. In: Physica A Statistical Mechanics and its Applications 392, pp. 3698–3707. doi: 10.1016/j.physa.2013.04.012. arXiv: 1108.0099 [q-fin.GN]. Forró, Z. (2015). “Detecting Bubbles in Financial Markets: Fundamental and Dynamical Approaches”. In: p. 95. doi: 10.3929/ethz-a-010510872. url: http://www.er.ethz. ch / content / dam / ethz / special - interest / mtec / chair - of - entrepreneurial - risks-dam/documents/dissertation/thesis%7B%5C_%7Dzalan%7B%5C_%7Dforro% 7B%5C_%7Dfinal.pdf. Geng, Y. and Luo, X. (2019). “Cost-sensitive convolutional neural networks for imbalanced time series classification”. In: Intelligent Data Analysis 23.2, pp. 357–370. Geraskin, F. (2013). “Everything you always wanted to know about log-periodic power laws for bubble modeling but were afraid to ask”. In: The European Journal Of Finance 19.5, pp. 366–391. Goodfellow, I., Bengio, Y., and Courville, A. (2016). Deep Learning. http : / / www . deeplearningbook.org. MIT Press. Gürkaynak, R. S. (2008). “ECONOMETRIC TESTS OF ASSET PRICE BUBBLES: TAKING STOCK*”. In: Journal of Economic Surveys 22.1, pp. 166–186. doi: 10 . 1111/j.1467- 6419.2007.00530.x. eprint: https://onlinelibrary.wiley.com/doi/pdf/10.1111/j.1467- 6419.2007.00530.x. url: https://onlinelibrary. wiley.com/doi/abs/10.1111/j.1467-6419.2007.00530.x. Harrison, J. M. and Kreps, D. M. (1978). “Speculative Investor Behavior in a Stock Market with Heterogeneous Expectations*”. In: The Quarterly Journal of Economics 92.2, pp. 323–336. doi: 10.2307/1884166. eprint: /oup/backfile/content_public/ journal/qje/92/2/10.2307/1884166/2/92-2-323.pdf. url: http://dx.doi.org/ 10.2307/1884166. He, H. and Garcia, E. A. (2009). “Learning from Imbalanced Data”. In: IEEE Trans. on Knowl. and Data Eng. 21.9, pp. 1263–1284. issn: 1041-4347. doi: 10.1109/TKDE. 2008.239. url: https://doi.org/10.1109/TKDE.2008.239. He, K. et al. (2015). “Delving deep into rectifiers: Surpassing human-level performance on imagenet classification”. In: Proceedings of the IEEE international conference on computer vision, pp. 1026–1034. Hochreiter, S. (1991). “Untersuchungen zu dynamischen neuronalen Netzen”. In: Diploma, Technische Universität München 91.1. Hochreiter, S. and Schmidhuber, J. (1997). “Long short-term memory”. In: Neural computation 9.8, pp. 1735–1780. Horák, J. and Smid, M. (2009). “On tails of stock returns: Estimation and comparison between stocks and markets”. In: Available at SSRN 1365229. Huang, W. et al. (2010). “Return Reversals, Idiosyncratic Risk, and Expected Returns”. In: The Review of Financial Studies 23.1, pp. 147–168. doi: 10.1093/rfs/hhp015. eprint: /oup/backfile/content_public/journal/rfs/23/1/10.1093_rfs_hhp015/ 1/hhp015.pdf. url: http://dx.doi.org/10.1093/rfs/hhp015. Jacobsson, E. (2009). “How to predict crashes in financial markets with the Log-Periodic Power Law”. In: Master diss., Department of Mathematical Statistics, Stockholm University. Japkowicz, N. and Stephen, S. (2002). “The Class Imbalance Problem: A Systematic Study”. In: Intell. Data Anal. 6.5, pp. 429–449. issn: 1088-467X. url: http://dl.acm. org/citation.cfm?id=1293951.1293954.

Johansen, A. and Sornette, D. (2002). “Endogenous versus Exogenous Crashes in Financial Markets”. In: arXiv e-prints, cond-mat/0210509, cond–mat/0210509. arXiv: condmat/0210509 [cond-mat.stat-mech]. Johansen, A. and Sornette, D. (2004). Endogenous versus exogenous crashes in financial markets, in press in “Contemporary Issues in International Finance”. Johansen, A. (2004). “Origin of crashes in three US stock markets: shocks and bubbles”. In: Physica A: Statistical Mechanics and its Applications 338.1-2, pp. 135–142. Johansen, A., Ledoit, O., and Sornette, D. (1998). “Crashes as Critical Points”. In: arXiv e-prints, cond-mat/9810071, cond–mat/9810071. arXiv: cond - mat / 9810071 [cond-mat]. Johansen, A. and Sornette, D. (1999). “Critical Crashes”. In: arXiv e-prints, condmat/9901035, cond–mat/9901035. arXiv: cond-mat/9901035 [cond-mat.stat-mech]. – (2010). “Shocks, Crashes and Bubbles in Financial Markets”. In: Brussels Economic Review 53.2, pp. 201–253. url: https://EconPapers.repec.org/RePEc:bxr:bxrceb: 2013/80942. Johansen, A., Sornette, D., and Ledoit, O. (1999). “Predicting Financial Crashes Using Discrete Scale Invariance”. In: arXiv e-prints, cond-mat/9903321, cond–mat/9903321. arXiv: cond-mat/9903321 [cond-mat]. Karim, F. et al. (2018). “LSTM fully convolutional networks for time series classification”. In: IEEE Access 6, pp. 1662–1669. Keynes, J. M. (1936). The General Theory of Employment, Interest and Money. 14th edition, 1973. Macmillan. url: https : / / cas2 . umkc . edu / economics / people / facultypages/kregel/courses/econ645/winter2011/generaltheory.pdf. Kingma, D. P. and Ba, J. (2014). “Adam: A method for stochastic optimization”. In: arXiv preprint arXiv:1412.6980. Kinouchi, O. and Copelli, M. (2006). “Optimal dynamical range of excitable networks at criticality”. In: Nature Physics 2, 348 EP -. url: https://doi.org/10.1038/nphys289. Kuramoto, Y. (1975). “International symposium on mathematical problems in theoretical physics”. In: Lecture notes in Physics 30, p. 420.

Ljung, G. M. and Box, G. E. P. (1978). “On a Measure of Lack of Fit in Time Series Models”. In: Biometrika 65.2, pp. 297–303. issn: 00063444. url: http://www.jstor. org/stable/2335207. Maimon, O. and Rokach, L. (2005). “Data mining and knowledge discovery handbook”. In: Mandelbrot, B. (1963). “The Variation of Certain Speculative Prices”. In: The Journal of Business 36. url: https://EconPapers.repec.org/RePEc:ucp:jnlbus:v:36:y: 1963:p:394. Martın Abadi et al. (2015). TensorFlow: Large-Scale Machine Learning on Heterogeneous Systems. Software available from tensorflow.org. url: http://tensorflow.org/. McClelland, J. L., Rumelhart, D. E., Group, P. R., et al. (1986). “Parallel distributed processing”. In: Explorations in the Microstructure of Cognition 2, pp. 216–271. McCulloch, W. S. and Pitts, W. (1943a). “A logical calculus of the ideas immanent in nervous activity”. In: The bulletin of mathematical biophysics 5.4, pp. 115–133. McCulloch, W. S. and Pitts, W. (1943b). “A logical calculus of the ideas immanent in nervous activity”. In: The bulletin of mathematical biophysics 5.4, pp. 115–133. issn: 1522-9602. doi: 10.1007/BF02478259. url: https://doi.org/10.1007/BF02478259. Miller, E. M. (1977). “Risk, Uncertainty, and Divergence of Opinion”. In: The Journal of Finance 32.4, pp. 1151–1168. issn: 15406261. doi: 10.1111/j.1540-6261.1977. tb03317.x. arXiv: 00368075. Miller, M. and Modigliani, F. (1961). “Dividend Policy, Growth, and the Valuation of Shares”. In: The Journal of Business 34. url: https : / / EconPapers . repec . org / RePEc:ucp:jnlbus:v:34:y:1961:p:411. Minsky, H. P. (1982). Can "it" happen again? : essays on instability and finance / Hyman P. Minsky. English. M.E. Sharpe Armonk, N.Y, xxiv, 301 p. : isbn: 0873322134. Nielsen, M. (2017). Neural Networks and Deep Learning. http://neuralnetworksanddeeplearning. com/. Olah, C. (2015). Understanding LSTM Networks. url: https://colah.github.io/ posts/2015-08-Understanding-LSTMs/.

Olver, F. W. et al. (2010). NIST handbook of mathematical functions hardback and CD-ROM. Cambridge university press. Parens, R. and Bar-Yam, Y. (2016). “Step by Step to Peace in Syria”. In: arXiv e-prints, arXiv:1602.06835, arXiv:1602.06835. arXiv: 1602.06835 [physics.soc-ph]. Potts, R. B. (1952). “Some generalized order-disorder transformations”. In: Mathematical proceedings of the cambridge philosophical society. Vol. 48. 1. Cambridge University Press, pp. 106–109. Rosenblatt, F. (1962). Principles of neurodynamics; perceptrons and the theory of brain mechanisms. Spartan Books. Shiller, R. (1981). “Do Stock Prices Move Too Much to be Justified by Subsequent Changes in Dividends?” In: American Economic Review 71.3, pp. 421–36. url: https: //EconPapers.repec.org/RePEc:aea:aecrev:v:71:y:1981:i:3:p:421-36. – (2015). Irrational Exuberance. 3rd ed. Princeton University Press. url: https:// EconPapers.repec.org/RePEc:pup:pbooks:10421. Shleifer, A. and Vishny, R. W. (1997). “The Limits of Arbitrage”. In: Journal of Finance 52.1. Reprinted in Harold M. Shefrin, ed., Behavioral Finance, Edward Elgar Publishing Company, 2001. Reprinted in Richard Thaler, ed., Advances in Behavioral Finance Vol. II, Princeton University Press and Russell Sage Foundation, 2005., pp. 35–55. Smith, L. N. (2018). “A disciplined approach to neural network hyper-parameters: Part 1–learning rate, batch size, momentum, and weight decay”. In: arXiv preprint arXiv:1803.09820. Sornette, D. (2003). Why Stock Markets Crash - Critical Events in Complex Financial Systems. Princeton University Press, p. 81. Sornette, D. and Cauwels, P. (2014). “Financial Bubbles: Mechanisms and Diagnostics”. In: 2. url: https://www.researchgate.net/publication/261475298_Financial_ Bubbles_Mechanisms_and_Diagnostics. Sornette, D., Cauwels, P., and Smilyanov, G. (2017). “Can We Use Volatility to Diagnose Financial Bubbles? Lessons from 40 historical bubbles”. en. In: Quantitative Finance and Economics. issn: 2573-0134.

Sornette, D. and Johansen, A. (2002). “Large stock market price drawdowns are outliers”. In: Journal of Risk 4. doi: 10 . 21314 / JOR . 2002 . 058. url: https : / / www . risk.net/journal-risk/2161095/large-stock-market-price-drawdowns-areoutliers. Sornette, D., Johansen, A., and Bouchaud, J.-P. (1996). “Stock Market Crashes, Precursors and Replicas”. In: Journal de Physique I 6.1, pp. 167–175. issn: 1155-4304. doi: 10.1051/jp1:1996135. url: http://dx.doi.org/10.1051/jp1:1996135. Sornette, D., Woodard, R., et al. (2013a). “Clarifications to questions and criticisms on the Johansen–Ledoit–Sornette financial bubble model”. In: Physica A: Statistical Mechanics and its Applications 392.19, pp. 4417–4428. doi: 10.1016/j.physa.2013. 05.0. url: https://ideas.repec.org/a/eee/phsmap/v392y2013i19p4417-4428. html. – (2013b). “Clarifications to questions and criticisms on the Johansen–Ledoit–Sornette financial bubble model”. In: Physica A: Statistical Mechanics and its Applications 392.19, pp. 4417–4428. Swets, J. A. (1988). “Measuring the accuracy of diagnostic systems”. In: Science 240.4857, pp. 1285–1293. Taylor, S. J. (2011). Asset price dynamics, volatility, and prediction. Princeton university press. Thurner, S., Farmer, J. D., and Geanakoplos, J. (2012). “Leverage causes fat tails and clustered volatility”. In: Quantitative Finance 12.5, pp. 695–707. Tirole, J. (1985). “Asset Bubbles and Overlapping Generations”. In: Econometrica 53.6, p. 1499. issn: 00129682. doi: 10 . 2307 / 1913232. url: http : / / www . jstor . org / stable/1913232?origin=crossref. Warusawitharana, M. (2018). “Time-varying volatility and the power law distribution of stock returns”. In: Journal of Empirical Finance 49, pp. 123–141. Weatherall, J. O. (2013). The physics of wall street: a brief history of predicting the unpredictable. Houghton Mifflin Harcourt. Yang, Q. (2006). “Stock Bubbles, Theory and Estimation”. In: December. url: http: //citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.426.9149&rep=rep1& type=pdf.

Yichuan, J. (2014). jd8001/LPPL. url: https://github.com/jd8001/LPPL. Zhou, W.-X. and Sornette, D. (2007a). “Self-organizing Ising model of financial markets”. In: The European Physical Journal B 55.2, pp. 175–181. issn: 1434-6036. doi: 10.1140/epjb/e2006- 00391- 6. url: https://doi.org/10.1140/epjb/e2006- 00391-6. Zhou, W.-X. and Sornette, D. (2007b). “Self-organizing Ising model of financial markets”. In: The European Physical Journal B 55.2, pp. 175–181